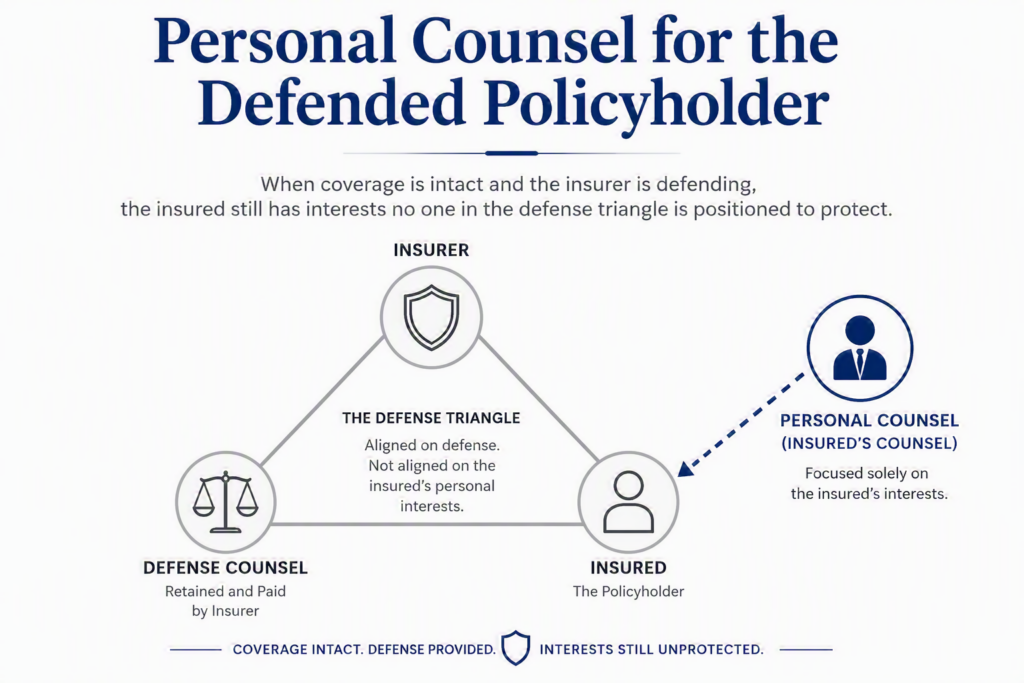

When coverage is intact and the insurer is defending, the insured still has interests no one in the defense triangle is positioned to protect.

Key Takeaways

- This article discusses the role of Personal Counsel for the Policyholder even when an insurer is defending, highlighting that coverage does not fully protect insured interests.

- Personal counsel helps monitor coverage, ensures the insured understands their obligations, and addresses potential excess exposure risks.

- Insurer-appointed counsel may face conflicts of interest, as they represent both the insured and the insurer; personal counsel serves to advocate exclusively for the insured’s interests.

- Personal counsel facilitates settlement discussions and preserves the record for potential bad-faith claims against the insurer for failing to settle within limits.

- If the insurer refuses to settle, personal counsel may explore options like § 537.065 agreements to manage the insured’s exposure to judgments.

Introduction

Much of the writing on personal or independent counsel for an insured assumes a coverage fight: the carrier has denied a defense, reserved its rights, or sued for a declaration of non-coverage, and the insured needs a lawyer of their own to navigate the conflict. This article addresses a quieter and far more common situation — the insured who has coverage and is being defended, with no present coverage dispute, yet whose interests still require independent attention. The reservation-of-rights and no-coverage scenarios raise distinct problems and are left for separate treatment. The point here is narrower and easily missed: a defended, covered policyholder is not the same as a fully protected one.

The gap arises because the insurer and the insured share an interest in defeating the claim but part ways on what happens if the claim has value. The carrier’s exposure is capped at its limits; the insured’s is not. When a case carries the realistic potential of a verdict above the policy limits, the insured’s personal assets are at risk in a way the carrier’s balance sheet is not — and the decisions that govern that exposure, chiefly whether and when to settle within limits, are made by the carrier, not the insured. Personal counsel exists to give the policyholder an advocate whose only loyalty is to the policyholder.

I. The Tripartite Relationship and the Limits of Appointed Counsel

Insurer-appointed defense counsel occupies a familiar but awkward position. The regularity with which this arrangement is used, and the ethical conduct of defense lawyers, sometimes make us forget that, despite being common and workable, it is an arrangement in tension with diverse competing interests. Counsel retained by the carrier to defend the insured owes professional duties to the insured as the client, yet is selected, paid, and — in practical terms — repeatedly retained by the insurer. Counsel is also often directed in how to conduct the defense by insurer-specific litigation management guidelines and insurer decision-making. Most of the time, the arrangement works because the carrier and the insured want the same outcome: a successful defense. The strain appears in a few areas, but most prominently at the settlement decision. Appointed counsel reports the case to the carrier and makes recommendations, but the authority to accept or reject a demand, and to commit the carrier’s money, rests with the adjuster. Appointed counsel is not positioned to press the carrier to protect the insured from an excess judgment with the single-mindedness that the insured’s own lawyer can bring.

Personal counsel supplies that voice. The role is to monitor the case from the insured’s point of view and to step in where the insured’s distinct interests are at stake. What personal counsel should not do is duplicate defense counsel’s work or engage in Monday-morning quarterbacking.

II. Confirming and Monitoring Coverage While the Defense Proceeds

That coverage is not in dispute at the outset does not mean it will stay that way. Personal counsel should obtain and read the policy rather than the declarations alone, confirm the structure of the limits, and determine whether defense costs erode the available indemnity — a wasting, or “burning-limits,”policy shrinks the very fund a within-limits settlement depends on. Counsel should also watch for coverage defenses that ripen as discovery develops: late notice, or an exclusion that becomes relevant once the facts are known. A carrier that is defending today can reserve its rights tomorrow. Treating “no coverage issue” as a present-tense observation rather than a settled fact is part of protecting the insured. Part of representing the insured is also making sure the insured understands the ongoing nature of their obligations under the insurance contract. The insured should understand the cooperation clause and other duties and should fulfill those obligations to ensure continued coverage and the best outcome of the case.

III. Engaging Appointed Counsel and the Carrier

A. Learning the case

Personal counsel’s first substantive task is to understand the matter as appointed counsel the carrier see it: the evaluation of liability and damages, the realistic verdict range, the probability and magnitude of a result above limits, the projected allocation of fault under Missouri’s pure comparative fault regime and the facts that make the case better or worse than it looks on paper.

B. Informing the carrier

Where the case carries excess potential, personal counsel should facilitate, to the extent possible, that the carrier has everything it needs from the insured to evaluate the claim. If defense counsel has evaluated the case as one of excess exposure, this job is easy, and documenting the insured’s wishes for resolution is straightforward. When excess exposure is not within the valuation of defense counsel or the carrier, but the insured and personal counsel believe there is excess exposure, this should be documented. To the extent possible, personal counsel should inform and educate the insurer about the exposure its insured faces and the insured’s demand that the case be settled within limits. This serves two ends at once. It moves the carrier toward a reasonable resolution, and it builds a record — documented, dated, and complete — of what the beneficiary of the insurance contract wanted and when. Given the fiduciary standard of conduct required of insurance companies that have control of the right to defend and settle, that record matters if the carrier later declines a within-limits opportunity.

IV. Facilitating Settlement Within Limits

The protective core of the engagement is making sure the insured gets the benefit of a settlement within limits when one is available. Personal counsel works to see that a reasonable within-limits demand is presented, and that the carrier has a genuine opportunity — and adequate time — to accept it. Counsel should confirm whether the policy contains a consent-to-settle provision, understand the insured’s own wishes, and account for any obstacles.

V. Relationship with Defense Counsel

Personal counsel’s relationship with appointed defense counsel matters. They share a client: the insured. But defense counsel also operates within a defense arrangement controlled and funded by the insurer, where the insurer and insured often have common interests but may diverge on settlement, coverage implications, file materials, or excess exposure. Personal counsel should recognize that tension without turning defense counsel into the target of every disagreement with the carrier.

The better approach is cooperative and direct. Personal counsel should treat defense counsel professionally, ask for their liability, causation, damages, and verdict-range evaluations, and use those evaluations to understand the case from the defense side. If the dispute is really with the insurer’s decisions or claims-handling position, personal counsel should direct the dispute to the insurer or the insurer’s separate counsel. Defense counsel should be brought into the dispute only when the issue actually involves defense counsel’s own conduct, obligations, or file.

For example, if personal counsel requests pre-suit or pretrial evaluations and defense counsel does not produce them, the first question should be practical: do the documents exist, and are they in the file defense counsel received or created? If the documents exist but defense counsel says they cannot provide them, the dispute belongs with the insurer. Personal counsel can explain the insured’s entitlement to the materials and demand production from the carrier without threatening defense counsel. Blaming defense counsel rarely improves the insured’s position, especially when defense counsel is already navigating two clients who disagree about access to documents.

The objective is not to create friction inside the defense team; it is to protect the insured’s separate interests while preserving the working relationship needed to resolve the case as favorably as possible.

VI. Preserving the Bad-Faith Record

If the carrier refuses a reasonable opportunity to settle within limits and an excess judgment follows, Missouri recognizes the insured’s claim against the insurer for bad-faith failure to settle and the insured’s recovery can include the amount of the judgment in excess of the policy limits. Personal counsel’s task is to preserve the record that would support one if the carrier’s conduct warrants it: the within-limits opportunities the carrier declined, the completeness of the information before it, the time it had to act, and any excess-exposure knowledge. This assignment has limitations, as personal counsel and the insured do not control the defense. However, personal counsel often has communications with counsel for plaintiff, defense counsel, and the insurer. Personal counsel should also have access to information and evaluation about the case from defense side. Personal counsel can use this information to communicate to the insurer the insured’s view of the exposure and risks in light that facilitates resolution, and preserves the insured’s rights.

VI. When the Carrier Will Not Settle: § 537.065, the Delayed Prosecution Agreement and Alternative Ideas.

Where excess exposure is real and the carrier will not pay to settle within limits, the insured is not without options. Missouri practice has long recognized arrangements that let an insured facing a judgment manage personal exposure while preserving the claimant’s path to the insurance. The familiar vehicle is the agreement under § 537.065, RSMo, whose defining feature is that it limits the claimant’s recovery to specified assets — typically the available insurance. That limitation is also what brings the agreement within the statute and triggers the insurer’s right to notice and to intervene. A different vehicle, the delayed prosecution agreement (DPA), does not limit recovery to specified assets and therefore falls outside the statute.

Despite the availability of these options, they are often unattractive to insured clients or plaintiff’s counsel. One of the significant results of modifications to § 537.065, RSMo. is that defendants with significant assets including individuals, trusts, businesses and public entities have lost the safe harbor the statute provided in the face of bad conduct by the insurer. Now, defendants cannot limit collection to specific assets without granting their opponent, the insurer, the right to contest the claim as a real party in interest. Even where the insurer has lost the coverage argument and was thus in breach the insurer now has the right to not only defend its own interests but to contest its insured’s positions, and the ability to prevent settlement of the claim. These new rights tip the scales in favor of the insurer and fly in the face of established contract law. As a result of these changes, it is harder to obtain a § 537.065, RSMo. even when an insured client would want such an agreement.

This poses new challenges to insureds facing insurer misconduct. Personal counsel may not be able to protect an insured using these once common devices. In some cases, the only option is to ride out the case and deal with an excess judgment after it has become a reality. Depending on the case, and the client, personal counsel should also consider referring the client to an asset protection attorney, or to bankruptcy counsel for further consultation once it becomes clear that the exposure is large, and the insurer has no intention of settling.

Conclusion

The defended policyholder is easy to overlook. Coverage is in place, a defense is underway, and the file appears to be in good hands. But the interests most likely to be underserved in that posture — protection against an excess judgment and the right to the benefit of a within-limits settlement — belong to the insured alone, and the defense structure is not designed to champion them. Personal counsel fills that role: confirming and monitoring coverage, measuring the exposure, holding the carrier to a fair opportunity to settle, and advising the insured on available options if a judgment looms.

For further reading on adjacent topics: